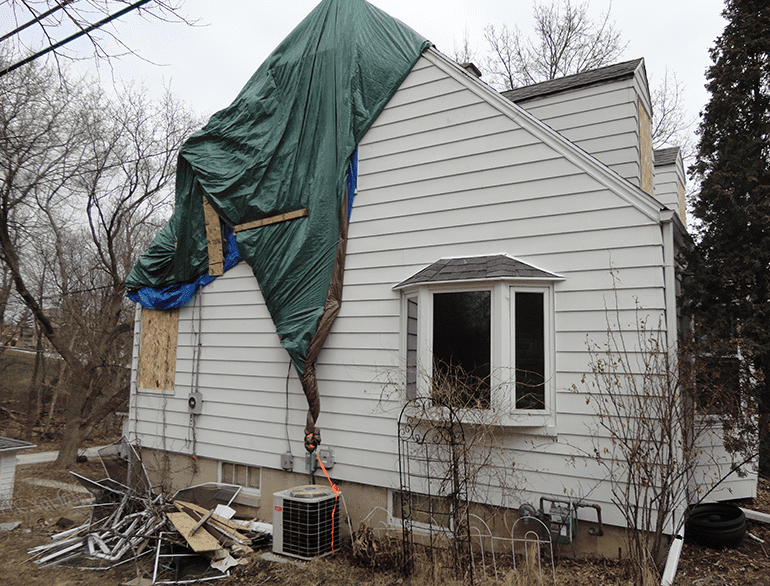

Fmv Before Loss Roof Repair

Part Three The Value Of Accurate Roof Age In Claims

Homeowners Guide On How To Get Your Insurance To Pay For Roof Replacement Roofcalc Org

Insurance Loss Claims State Roofing Company Of Texas

Is Storm Damage Tax Deductible Servpro Of Denver West

Hail And Storm Damage Coty Construction

Homeownership Rate Backslides To Near Its 48 Year Low Home Buying Home Ownership Home Protection

In most cases the fmv of your property after the casualty event is equal to the fmv immediately before the event less the cost of the repairs necessary to restore it to its original condition.

Fmv before loss roof repair.

Car Buying Contract Template Beautiful Sample Vehicle Purchase Agreement 19 Documents In Pdf Word In 2020 Contract Template Purchase Agreement Car Purchase

Mokan Home Improvement Llc Roofing Contractor

Hail Damage Roof Repair Cost Insurance Claim Process

How Can I Spot A Disreputable Company Praus Roofing And Construction

Solar Panels And Roof Damage What You Need To Know Energysage

Insider Tip Actual Cash Value Vs Replacement Cost Insurance Twfg Insurance Services

Replacement Cost Value Rcv Vs Actual Cash Value Acv

How Do You Determine The Value Of An Inherited Home Bankrate Com

Casualty Loss Tax Deduction Can You Take It Credit Karma Tax

What Is And Isn T Covered By Homeowners Insurance

Car Buying Contract Template Beautiful Sample Vehicle Purchase Agreement 19 Documents In Pdf Word In 2020 Contract Template Purchase Agreement Car Purchase

What Exactly Is Actual Cash Value Expert Commentary Irmi Com

Insider Tip Actual Cash Value Vs Replacement Cost Insurance Twfg Insurance Services

2020 Costs For Tpo Roofing Installation Membrane Prices Insulation Options Top Manufacturers Roofcalc Org

Ixmz9st0e9urjm

What Actually Hurts A Home Appraisal Homego

Smart Moves When Buying A Foreclosed Home Interest Com

What Every Seller Needs To Know About The Home Appraisal Process

Apartment Addition Or In Law Suite What It Costs And How To Pay For It

Selling Your Home With An Open Insurance Claim Cohen Law Group Orlando Attorneys

How To Calculate Fair Market Value Of Property Millionacres

:max_bytes(150000):strip_icc()/GettyImages-599380288-593766c53df78c537bbdb503.jpg)

Introduction To Valued Policy Law Vpl

Tax Treatment Of Casualty Losses And Casualty Gains From The 2017 Hurricanes By Arkadiy Eric Green Cpa Berkowitz Pollack Brant Advisors And Accountants

Https Fhlb Com Resourcecenter Documents Community Housing Programs Fhlbd Ahp Rental Workbook Pdf

Source : pinterest.com